Labor

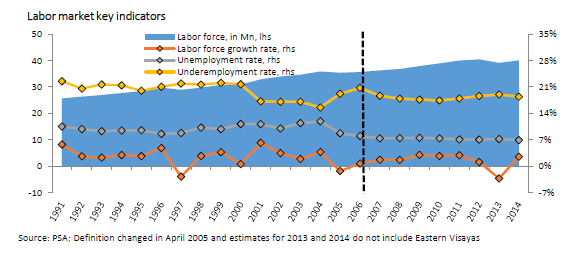

With a population of nearly 100 million growing at 2%, the Philippine economy needs to create many more jobs, as well as better quality jobs, than it has been doing. The size of the labor force as of July 2010 was 39 million, out of an estimated 61 million population aged 15 years and over. Of this total, some 36 million persons were employed. The unemployment rate stood at 6.9 percent, representing 2.7 million persons, and the underemployment rate was 17.9 percent, representing 6.5 million persons. Over nine million Filipinos would like to work more or would like to have some work, either full or part time (see Figure 180).

View original figure here

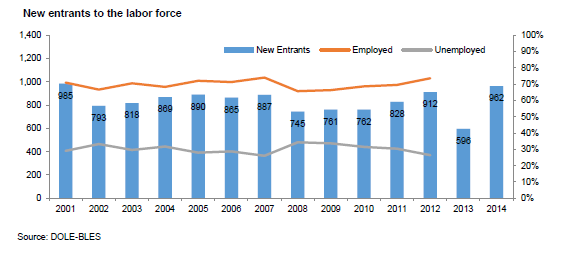

Filipinos who enter the workforce each year averaged 846,000 for the past decade (see Figure 181). The economy does not create enough quality jobs to employ them all. Some of those seeking jobs instead go abroad to join the more than 8 million Filipino immigrants and overseas workers, while others remain unemployed and underemployed in the Philippines, often assisted by remittances from relatives working abroad.222 A significant percentage of college graduates cannot find employment until some years after they leave school; 19% of the unemployed in 2009 were college graduates (see Figure 16). Without the demand for Filipino employment overseas, the country’s unemployment and underemployment rates could be two to three times higher.

View original figure here

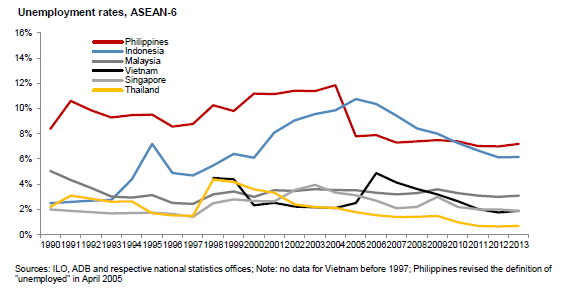

View original figure hereIndonesia and the Philippines have the highest unemployment rates among the ASEAN-6 (see ). The other four ASEAN-6 had employment rates at around four percent and below with Thailand at two percent.

View original figure here

View original figure hereFigure 183 shows that the Philippines has the highest brain drain of the ASEAN-6, with Singapore, Indonesia, Malaysia, and Thailand ranked among the top 30% of the 139 countries covered in the Global Competitiveness Survey. A reason for the low rank of the Philippines is that the economy does not provide sufficient jobs to allow them to remain at home.

Longstanding emigration relationships with Australia, Canada, New Zealand, and the US and their English-speaking skills provide many Filipinos with better access to foreign job opportunities than workers in the other ASEAN-6 economies.

View original figure here

View original figure hereSome find employment abroad because they lack the skills for locally available jobs. For example, in the BPO sector demand for qualified applicants is very high, but only a few qualify. While a customer relations agent in Manila earns as much as a household help in Hong Kong, a Filipino in the latter category may lack the skills to qualify for BPO employment at home.

Despite considerable efforts undertaken by the private sector, education officials, and government, much remains to be done to match the educational and training curriculum to available jobs. In recent years awareness has increased of the need for schools to revise their curricula to address the mismatch of skills and jobs. Until this challenge is solved, inadequate skills (e.g. English, math, science, engineering, entrepreneurship, logical thinking, research, writing, and blue collar training) will prevent many young Filipinos from qualifying for available jobs in the private sector.

More young Filipinos need to acquire specialized fields related to the Seven Big Winner sectors, especially in agribusiness, creative industries, manufacturing, and mining. The fast-growing BPO sector, which is expected to hire 100,000 more employees in 2010 (and require commensurate new office space), would grow even faster if new college graduates and older applicants had better skills.

The Department of Labor (DOLE) is undertaking Project Jobs Fit to identify the new, emerging employment sectors for the next decade and the skills needed for future jobs in these sectors.223 Educational institutions and other stakeholders should develop the curricula and teaching materials that will train students in order to increase their chances of being employed in the new sectors, thus reducing the job mismatch and unemployment.

The DOLE categorized the emerging employment sectors as (1) Key Employment Generators (KEGs), (2) Emerging Industries, (3) Hard-to-fill Occupations, (4) In-demand Occupations, and (5) Overseas Employment KEGs.

(1) Key Employment Generators

- Agribusiness

- Cyberservices

- Health and Wellness

- Hotel, Restaurant, and Tourism

- Mining

- Construction

- Banking and Finance

- Manufacturing

- Ownership Dwellings and Real Estate

- Transport and Logistics

- Wholesale and Retail Trade

- Overseas Employment

(2) Emerging Industries

- Creative Industries

- Diversified/Strategic Farming

- Power and Utilities

- Renewable Energy

(3) Hard-to-fill Occupations

- Agribusiness – Food processors/Food technicians

- Cyberservices – Animators

- Health and Wellness – Spa/Massage therapists

- Hotel, Restaurant, and Tourism – Cooks

(4) In-Demand Occupations

- Agribusiness – Aquaculturists

- Health and Wellness – Opticians

- Hotel, Restaurant, and Tourism – Bakers

(5) Overseas Employment KEGs

- Healthcare

- Building and Construction

- Petroleum/Oil and Gas/Energy

- Hotel, Restaurant, Tourism, and Gaming Industry

- IT/Cyberservices

- Manufacturing

- Seafaring

- Electronics

- Household Services

- Production and Production-related Work

Since job creation requires investment, the government should pursue high growth policies that maximize investment and improve productivity. This in turn will create better quality jobs in the formal sector that pay better, offer more job security, and yield increased payroll tax revenue for the BIR.

View original figure here

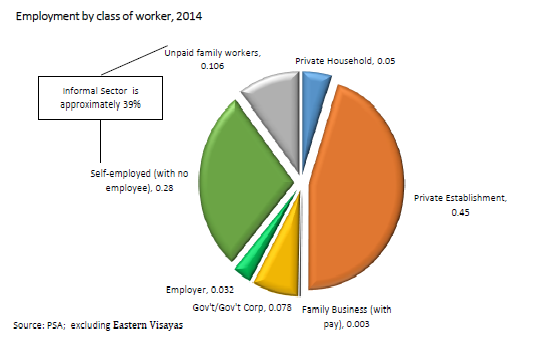

View original figure hereIn Figure 184, showing employment by class of worker, the informal sector was 42.6% of the workforce in 2009. By developing programs to improve the quality of jobs, policy makers hope to substantially increase the share of full-time employment with private firms from its current 39.4% of the workforce.

Minimum wages and holidays are discussed in Part 4 under Business Costs, and Part 3 Manufacturing and Logistics discusses the decline of Philippine export industries based on low-cost labor manufacturing in the Philippines. Investment in such manufacturing for export has concentrated within Asia over the last decade in China, Indonesia, and Vietnam. Falling tariffs from global and regional trade liberalization and weak anti-smuggling enforcement have exposed Philippine manufacturers to competition from cheaper imports in the domestic market, causing loss of market share for Philippines exports in international markets as well as for Philippine-produced goods in the domestic market. Consequently, hundreds of thousands of jobs in manufacturing have been lost.

However, with wages rising in the fast-growing coastal areas of China, manufacturers are moving inland, where wages are 30% less, or to other Asian countries. Potentially, millions of manufacturing jobs may shift away from these provinces in the next few years. The Philippines may be able to attract some of them to relocate to industrial estates in Central Luzon and Cebu if a competitive package for electricity, labor, and other operating costs can be created. The Clark/ Subic SEZs and Mactan, with their logistics connections and large populations, should be able to offer an opportunity to set up new zones with special incentives, such as discounts, for exporters who relocate to the Philippines and are willing to hire large numbers of workers.

The Philippine Labor Code is 36 years old, out of date, and out of tune with regional developments. Efforts to reform it have been objected to by militant labor groups and their allies in Congress, who advocate amendments that would make the Philippines less attractive to private sector investment relative to regional competitors. Foreign observers have commented that the statist advocacies of leftist groups in the Philippines have learned little from the success of China and Vietnam becoming integrated into the global logistic chain and attracting high volumes of FDI to build strong export manufacturing industries that have created millions of jobs.

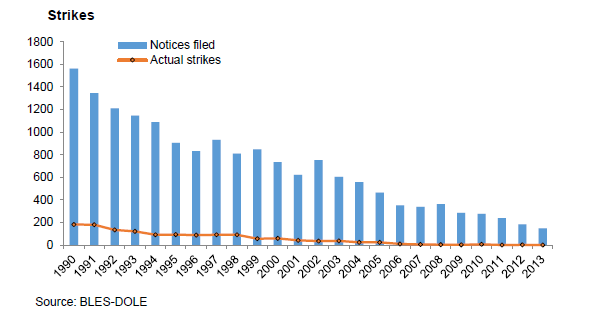

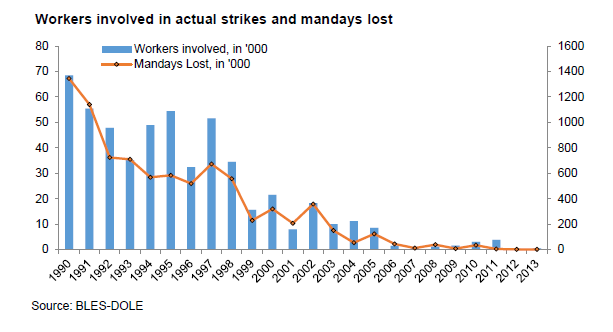

Disruptive labor action has almost disappeared in recent years, as shown in Figures 185 and 186. The incidence of labor strikes has declined steadily since a high in the years immediately after the fall of the dictator president Marcos in 1986. In recent years, very few actual strikes have taken place, and most lasted for only a few days. Notices of strikes have been much higher than actual strikes. However, preventive mediation action has usually resolved issues without workers going on the picket line. Increasingly, labor and management in the country have been able to resolve differences without the disruption of business operations.

View original figure here

View original figure here View original figure here

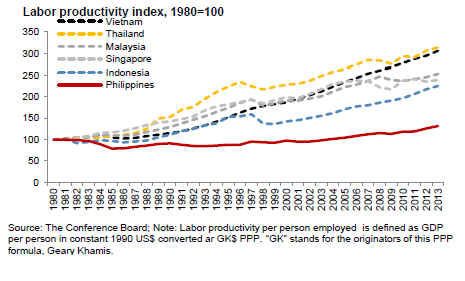

View original figure hereEconomists comment on the inability of the Philippine economy to raise labor productivity over many decades, as shown in Figure 187 comparing the Philippines within the ASEAN-6. All five of the other ASEAN economies have increased productivity since 1990. It more than doubled in Thailand and more than tripled in Vietnam. Productivity is GDP divided by the workforce.

View original figure here

View original figure hereAs a consequence of its comparatively high minimum wage (see Part 4 Business Costs) and flat productivity, the Philippines is low ranked among the ASEAN-6 in the pay and productivity category of the WEF Global Competitiveness Report (see Figure 188).

View original figure here

View original figure here

Headline Recommendations

- Modernize the Labor Code. Rationalize holidays. Allow overseas service firm workers compensatory days off. Maintain the flexible working arrangements introduced in recent years.

- Focus on improving labor productivity. Create several million new direct jobs and many more indirect jobs. Attract manufacturers relocating from China. Reduce the unemployment and underemployment rates.

- Continue to resolve differences without disruptive labor action. Allow selfregulation of companies with support of chambers of commerce and industry associations. Reform the NLRC. Further narrow the skill-jobs mismatch byrevising curricula and training. Re-introduce dual training system and support greater interaction between TESDA and private sector.

Recommendations: (9)

A. Modernize the 36-year old Labor Code to end the disadvantage it has created for the Philippines with regional competitors. Areas for possible amendment include allowing night work for women, making it easier to dismiss employees for sound business reasons and poor performance, non-diminution clause of wages and benefits and revising rules on labor contracting. (Medium-term action DOLE, DTI, Congress, trade unions, and private sector)

B. Rationalize holidays to approach ASEAN average of 15 paid days without reducing income of full time employees and increasing income of casual workers (see Part 4 Business Costs). (Medium-term action DOLE, OP, and Congress)

C. In order to increase competitiveness, continue to allow firms providing same day services to overseas clients toprovide employees, who have to work on Philippine holidays, substitute days off with pay in lieu of paying holiday premium.224 (Immediate action DOLE and private sector)

D. Make wage increase consistent with inflation and productivity. Redefine the basis for the minimum wage to take into account smaller families and more than one wage earner. Create industry-specific minimum wages. (Medium-term action DOLE, Tripartite Regional Wage Boards, Congress, and private sector)

E. Further narrow the skill-jobs mismatch by revising curricula and training and retraining the workforce and older students better for the hard-to-fill jobs of the present and future economy. Ensure that skills required for the successful growth of the Seven Big Winner Sectors are included in the curricula; involve the private sector in curriculum development and re-promote dual technical training.Support greater interaction between TESDA and the private sector. (Long-term action DOLE, DTI, DEPED, CHED, TESDA, Congress, and private sector)

F. Create millions of new jobs, many of higher quality, through increased investment. Reduce the annual shortage of jobs and give Filipinos better choices of domestic and overseas employment. (Immediate action all concerned public and private sector entities)

G. Develop a package of incentives to attract manufacturers relocating from China, with a target of creating several hundred thousand new jobs within five years. Promote the package to potential investors. (Immediate action DTI, DOF, DOLE, CEZ, SBMA, and private sector)

H. Maintain the low level of labor disruption of business operations through good communications and cooperation between labor and management. Allow self-regulation of companies with the support of chambers of commerce and industry associations. (Immediate action DOLE and private sector)

I. Improve the speed and fairness of the adjudication of labor cases before the National Labor Relations Commission (NLRC). (Immediate action DOLE and NLRC)

Footnotes

- Remittances to relatives in the Philippines are expected to reach US$ 20 billion in 2011.[Top]

- DOLE’s Bureau of Local Employment headed a multi-agency team that prepared a 200-plus page study available at https://ble.dole. gov.ph or at https://www.dole.gov.ph.[Top]

- This scheme is already in place and needs to be maintained. Companies are required to convince more than 50% of their employees to accept this scheme. When that is achieved, DOLE certifies.[Top]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}