With its archipelagic character, the Philippines depends on seaports much more than countries with large continuous landmass. Since a high percentage of domestic and international commerce and travel is by sea, the efficiency of maritime transportation has become increasingly essential to national competitiveness. The high cost of domestic marine transport has long been questioned, while the enormous potential for tourism (both domestic and international) is greatly influenced by the quality of seaports (as well as airports). Improving maritime safety is an important issue given the high loss of life from negligence of ship owners and government agencies, terrorism, and weather.

Figure 88: Container traffic per country, in Mn TEUs, 2004-2010

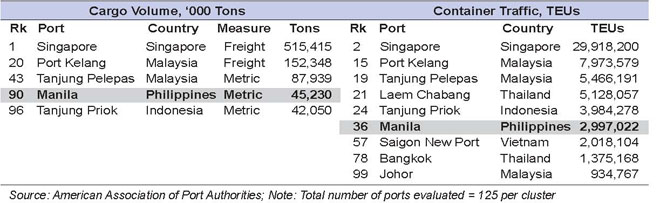

The volume of international container shipments in and out of the Philippines is low in comparison to Asia’s major export economies (see Figure 88). Total Philippine container traffic is less than 5 million TEUs and is growing very slowly. Singapore, Hong Kong, and Kaoshung ports handle over 20 million TEUs/year; Laem Chabang (Thailand) and K’lang (Malaysia) ports each handle about 5 million TEUs/year. The terminals at Manila (MICT and South Harbor) handle about 3 million TEUs/year. Manila is ranked 90th in the world in tonnage volume and ranked 36th in container traffic (see Table 40).

Over the last decade, there has been significant investment in the development of the international ports of Batangas, Cagayan de Oro (PHIVIDEC), Davao, and Subic. Their combined capacity has almost doubled. GRP agencies have borrowed from JBIC to develop the new ports in Batangas, Subic, and Cagayan de Oro and will need to generate substantial port revenues to pay these loans and to avoid the new facilities becoming white elephants.

Historically traffic has grown around 5% annually, but volume is projected to increase by only 2-3% until world trade has fully recovered from the financial crisis. While the new ports have considerable capacity for future growth, the volume share of the main NCR ports is not spread efficiently.

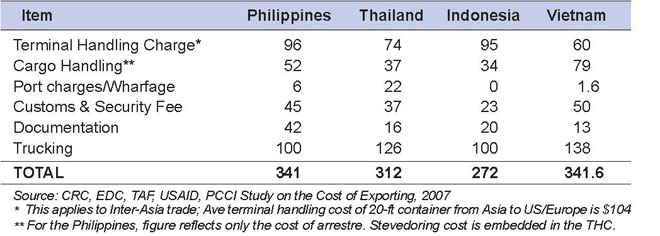

Table 41 shows costs of exporting a 20-foot container at ports in Indonesia, Philippines, Thailand, and Vietnam. Studies have shown both international and domestic shipping costs can be reduced by efficiency improvements and reduction or removal of unnecessary charges lacking added value, especially those by government.

In Manila there are two ports owned by the Philippine Ports Authority (PPA) – International Container Terminal Services Inc (ICTSI) and Asian Terminals Inc (ATI) – with operations awarded to private operators and one privately-owned and operated (Harbor Center). Harbor Center only handles non-containerized cargoes. Batangas and Subic handle very low TEU volumes. The present NCR port usage has created traffic problems, adding to the extreme congestion of Metro Manila, and a contributor to passenger and cargo traffic as well as industrial concentration in the capital (see Figure 89). Competition among port operators is limited, especially in foreign containerized cargoes.

Figure 89: Truckers, motorists in private vehicles, and drivers of

passenger jeepneys on their way to North Harbor

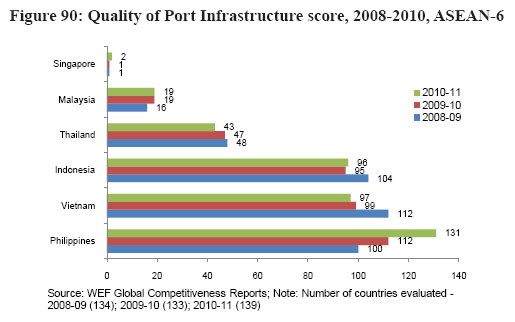

As Figure 90 shows, the quality of port infrastructure rank for the Philippines in the WEF Global Competitive Report is the lowest among the ASEAN-6. As an archipelago with a very large number of ports, the Philippines faces a challenge, only shared with Indonesia in Southeast Asia, to undertake reforms and large investments to modernize as many ports as possible.

As it expands, the Ro-Ro transport system introduced by President Macapagal Arroyo is increasingly giving passengers and shippers an alternative to traditional air and marine shipping (see Map 3).

Map 3: RO-RO Network

Domestic shipping can be divided into three categories with different port and infrastructure requirements: (1) pure containerized lift-on/lift-off (LOLO) shipping for long-haul routes between main ports; (2) large Roll-on/Roll-Off (RORO) ferries with passengers on long-haul routes; and (3) bulk (dry and wet), break bulk, and small container shipping.

The Philippine constitution limits foreign equity in public utilities (e.g. transport) to 40% maximum. The concept of consortium shipping (foreign ships can carry each other’s foreign cargoes within the Philippines) has been proposed as a means of increasing competition and lowering shipping costs.

Philippine ports suffer from a structural regulatory problem. The DOTC has limited jurisdiction over Special Economic Zone (SEZ) ports including Subic Bay Freeport Zone, Poro Point, and PHIVIDEC. Also, there is no uniform administration of RORO ports; some are under PPA, while others are under LGUs, and fees are not uniform. PPA is subject to political pressure to allocate funds for all ports, dissipating limited resources rather than developing major ports in a hub-and-spoke system.

{kind=link}

{kind=link}

{kind=link}

{kind=link}