Background (BPO)

<

<

Sector Background and Potential

“The Philippines can be the next India, with the right government support. The work ethic is strong, English skills are better. But the government should drive education araound technology.Now is the time to move forward, to drive growth and innovation. The Philippines is in a strong position to do that.”

—Scott Murray, Chair and CEO, Stream, an American BPO firm quoted in the Philippine Daily Inquirer on February 13, 2010; he said Stream plans to grow its Philippine workforce from 11,000 to 50,000.

Information technology and business process outsourcing (IT-BPO) is the fastest-growing employment and one of the highest revenue generating economic sector in the Philippines today.42 IT-BPO is the biggest of our Seven Big Winners, because of its current size, high growth rate, and potential to employ millions of Filipinos.

The sector originated from data-entry and software-writing services in the pre-Internet years and has grown exponentially during the past decade (see Figure 61). Beyond call center services (including customer relationship management and technical support), a wide variety of other business processes are fulfilled over the Internet or leased lines by providers in the Philippines. These include finance and accounting, creative services, billing and collections, document digitization and search engines, engineering design, financial and legal research, human resource management, medical transcription and coding, and publishing.

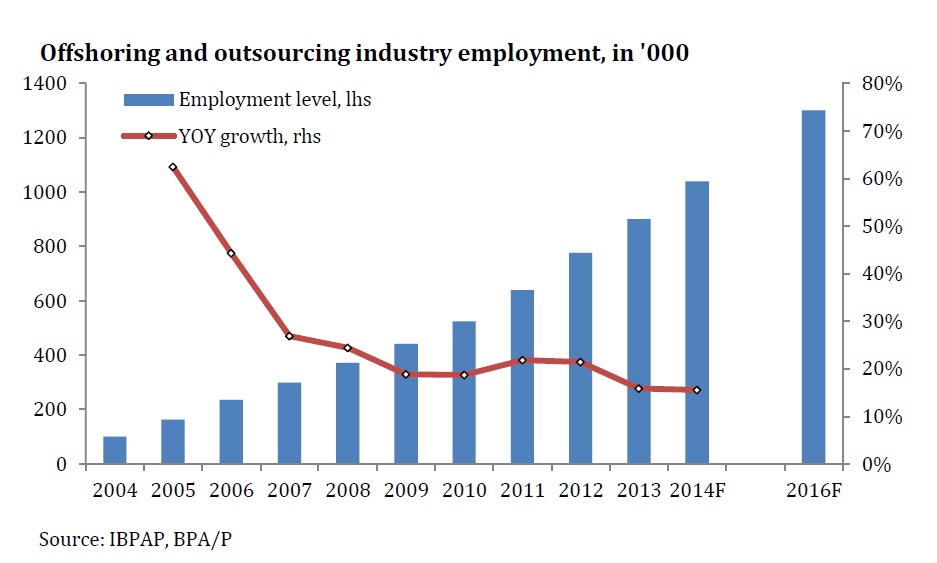

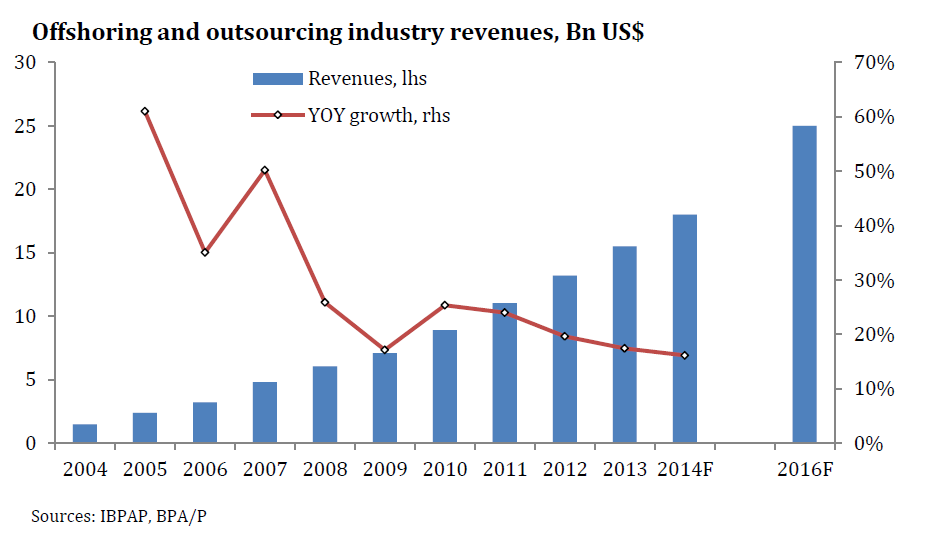

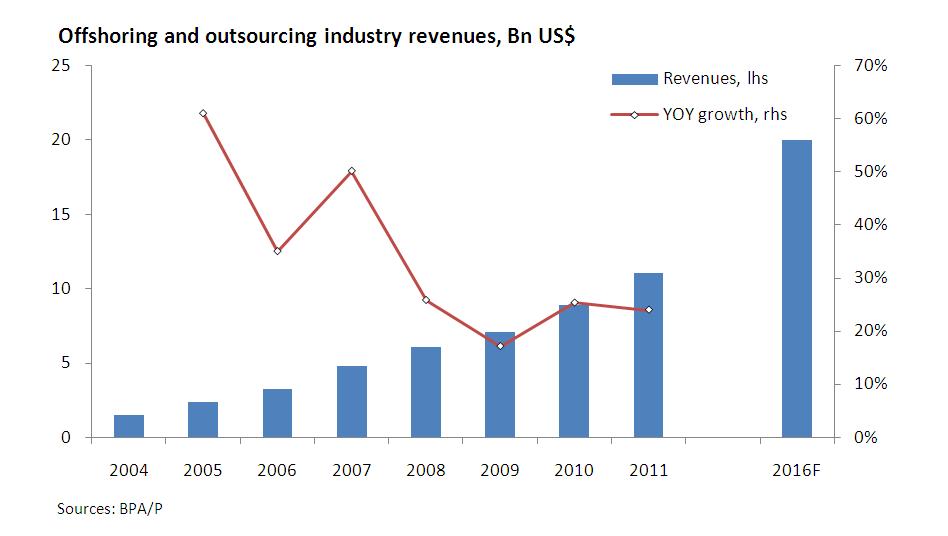

The global financial crisis slowed employment growth in the industry in 2008-2009 to a still rapid rate of 25% per annum after an extremely fast annual pace of 43% in the previous four years. As of 2009, 442,000 Filipinos are employed in the industry (of whom 70,000 entered the industry workforce in 2009), and annual revenues reached US$ 7.2 billion (see Figure 62) or some 4% of GDP and are growing at 36% annually. Within a few years, one million Filipinos could be working in the industry.

By 2008 (see Figure 63), the Philippines ranked second after India in the BPO industry outside North America, with 19% of the global offshore BPO market compared with India’s 45%. While the Philippines has only a tenth of India’s population, it has taken a fifth of the offshore market.

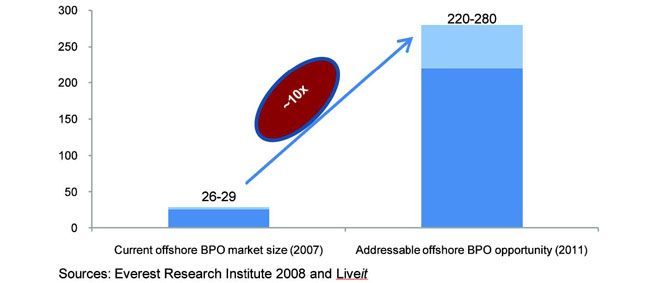

A leading industry research institute estimates current additional opportunities at over US$ 200 billion, eight times the value currently delivered from outside North America (see Figure 64). It is reasonable to describe industry potential in the decade ahead as capable of reaching as high as two million employees and US$ 30 billion in annual revenues. Non-voice employment is growing at a slightly faster rate than voice, and more and more large foreign firms are establishing in-house back-office operations in the country to join the outsourcing firms that are also here. Table 24 shows the rate of employment growth in 2009 of the IT-BPO subsectors showing that back-office or non-voice BPO is currently growing at 25% compared with call centers (23%).43

View original figure here

View original figure here

The Philippines has several clear advantages: a large workforce; a large pool of educated, English-speaking talent with a strong customer-service orientation and strong cultural affinity to North America; 450,000 college graduates annually; highly-reliable low-cost international telecommunications infrastructure; diverse and inexpensive suitable site locations; and strong government support. In addition, a survey by a leading industry expert showed call center operating costs in the Philippines in 2006 were roughly the same as in China and India and about 75% less than in the US.44

These key drivers for success must be sustained and country competitiveness strengthened. There are, however, challenges and reforms needed to realize the country’s high potential for continued growth.

Challenges and Issues

Legal Framework

There are four areas where the country’s legal framework requires attention and, in some cases, reform to help the IT-BPO sustain its global competitiveness. These are retention of current fiscal incentives schemes, the passage of three non-fiscal laws that the IT-BPO industry has identified as priority, labor legislation (current or proposed) that makes it more difficult for firms to compete in the global marketplace, and the practice of declaring non-working holidays.

First, on the current laws providing fiscal incentives to firms registered with PEZA and the BOI, these laws are instrumental in many investors’ decisions to set up operations in the Philippines. Almost all new IT-BPO locators establish their operations within PEZA zones in order to avail of initial tax holidays and low taxes after the expiration of their initial holidays. However, for several years, the Department of Finance (DOF) has worked with allies in the Senate to end these fiscal incentives. If DOF’s proposal to eliminate incentives becomes law, the growth of the industry could be substantially slowed.

Government would, on the other hand, benefit substantially from further and faster growth of the IT-BPO industry in many ways including taxes from employees. The income of employees is usually taxed at normal income-tax rates, and the 100,000 new workers who will be hired in 2010, for example, will add billions of new government revenue from income, Value Added Tax (VAT), and excise taxes.45

Second, the industry was disappointed that the 14th Philippine Congress failed to approve three new non-fiscal laws important to strengthening the legal framework of the industry: the Cyber Crime Prevention Act, the bill to create a Department of Information and Communications Technology (DICT), and the Data Privacy Act. The first two were approved by the House but had not completed the final stages of consideration in the Senate when the legislative session adjourned.

The Data Privacy Act did not pass the House, and a bill to remove the prohibition in the Labor Code against female employees working at night was introduced in the House but made little progress.

These four bills will be filed again in the 15th Congress and repeat the legislative process. However, having reached advanced stages in the 14th Congress, passage of the Cyber Crime Prevention and DICT bills should be faster, as committee hearings can be completed quickly.

A reason why these bills were not passed was insufficient understanding of the IT-BPO sector and the importance of these bills to the growth of the industry. Although the Commission on Information and Communications and Technology (CICT) and industry leaders actively sought their passage, the harmful effects of non-passage were not well appreciated by legislators.

The DICT bill will elevate the current CICT – the primary regulatory body for information and communications technology in the country established by an executive order – to department status, which most ASEAN countries have done. This will deter a future president from abolishing the commission by executive action.

The lack of legislation on data privacy is a growing cause of concern for prospective investors and a substantial hindrance to the development of the sector in the Philippines. In the 14th Congress the bill was reported out of committee in the Senate but not in the House. Yet English-speaking IT-BPO competitor countries like Malta have legislated data privacy laws.46 There is a real danger of losing investors to countries with a more favorable legislative framework for IT-BPO.

The absence of protection against data piracy is a key issue for IT-BPO companies that move large amounts of data across borders. The lack of punishment for violators is of great concern to stakeholders. Unfortunately, the importance and urgency of this issue is not understood by legislators.

The Philippines has existing laws including the E-commerce Act, the Consumer Protection Act and other trade and industry-related regulations, which arguably cover some concerns for data privacy. Though these laws do not address the entirety of the problem (they only cover about a fourth of what the data privacy bill covers), the sector can review and possibly amend these regulations in the meantime before the Data Piracy Act becomes law.

A “band-aid” solution could be created to at least address the primary concerns of industry stakeholders. A possible provisional solution may be to revise the IRRs of these laws through a DTI departmental order to address major issues of data piracy. Although guidelines alone do not have the authority to impose penalty provisions without legislation, revising the IRRs may help.47 Sometimes guidelines can also be the basis for future legislation. There should to be an industry sub-group to study this.

Another potential stopgap measure can be the Revised Penal Code (PD 1718) “Restricting the Use of Documents and Information Vital to the National Interest in Certain Proceedings and Processes.” The code is used by Philippine accounting firms to protect their clients from the misuse of information when subjected to peer reviews by foreign entities. However, though certain provisions in the code can offer such protection, overall it is not considered to be very strong in protecting data piracy.

The Philippine medical transcription industry, working with practitioners from the US, UK, New Zealand, India, and Caribbean countries, is preparing an “ethical best practices manual” that includes templates for service-level agreements, acceptable business practices, marketing, solicitations, and data privacy guidelines, which the sub-sector hopes can be used to further explain how it works.

These bills for the IT-BPO sector need more champions and advocates in the Congress to support the key sponsors of the legislation in the 14th Congress who are returning in the 15th Congress. However, there is weak public understanding that the IT-BPO sector directly and indirectly provides jobs and contributes to the overall development of the country, and therefore there is little or no support for legislative reform that would benefit the sector.

As a new sector growing rapidly, the public is not familiar with how IT-BPO work compares with more traditional sectors. Some issues unique to IT-BPO companies are misunderstood. People are easily swayed by misconceptions and unproven issues, sometimes aggravated by the media. Misperceptions of the industry can harm support in Congress.

Third, another challenge faced by the industry is that legislation originating in the Congressional labor committees is often not in its interest. Philippine labor laws are oriented towards manufacturing rather than the IT-BPO sector, understandably since the latter did not exist when the laws were made.

Some legislative proposals are motivated by abuses of smaller firms with lower standards that can be rectified without passing a law that may harm the whole industry. (multinational corporations) MNCs have high standards and do not follow the practices such bills are intended to stop. Dialogue among concerned parties in the private sector, government, and labor is the more appropriate solution to prevent such abuses; not new laws, such as the proposed security of tenure bill.

The position of most legislators tends to be pro-labor because they think populism wins them more votes in elections. But pro-business measures increase jobs, which are what many Filipinos need. There is a need for general public education to address this lack of understanding.

In the 14th Congress, the House Labor Committee chairman proposed to review and amend every book of the Labor Code. But while it would be ideal to modernize the Labor Code to be like Singapore’s, as a strategy it would be difficult to pass such a law. It is too easy for some groups to stop progressive legislation. Political resistance when amending the entire code is greater since a complete overhaul – compared with amending specific provisions – creates much more opposition. As a strategy, the best approach should be to focus on amending high-priority issues and not a complete revamp of the Labor Code.

The Department of Labor and Employment (DOLE) would like to form a tripartite council with the private sector and labor groups to revise parts of the Labor Code. This would consist of key government agencies, such as DOLE, and representatives of the private and labor sectors.

In amending the Labor Code, there are two key areas that the IT-BPO sector should focus on: subcontracting and termination of employment. There are proposed amendments to the Labor Code that would make it more difficult for employers to engage in subcontracting. The sector should advocate against this. In addition, the Labor Code should be amended to make it easier for companies to terminate employees in a reasonable manner.

Finally, the practice of declaring an excessive number of non-working holidays needs to be reviewed in the context of its effect on the productivity and competitiveness of Philippine firms. The Philippines has more non-working paid holidays than its country competitors. For the many firms in the industry operating nonstop, every holiday carries a cost for overtime and holiday pay (see Part 4 Business Costs).

New holidays have been legislated or declared (see box on the next page) without any consultation by the Congress or the Executive with the industry and other stakeholders and on extremely short notice, costing the industry millions of dollars of unbudgeted expenses for every holiday declared.

A new law to rationalize holidays should be considered that sets a limit on the total number of non-working holidays. The IT-BPO industry is unique in that its foreign clients observe different holidays than the Philippines and may require services to be provided on Philippine holidays. Rules should be made allowing these firms to pay regular wages for working on such days, as long as compensatory days off are given. Local city and provincial non-working holidays also add to business costs and affect industry competitiveness. Firms that export goods and services could be exempted in order to improve competitiveness.

India, which is the global IT-BPO leader and the Philippines’ main competitor, has in contrast increased worker productivity and its edge in labor cost over the Philippines by simply declaring a nine-hour workday. This is an example of how countries with more flexible labor laws will be better able to compete in today’s dynamic and hyper-competitive global marketplace. The Philippines will have to reform its legal and other systems with urgency if it wants to sustain its competitive advantage and remain a serious player in the global IT-BPO space.

Labor Supply

According to BPAP, the industry has experienced increasing employment growth rates from 2004 to 2007 for back-office processes and software development at average rates of 60% and 33% respectively, while voice-based services had a declining growth rate, although still averaging 52% in the same timeframe.

A robust talent supply is needed to sustain this growth, but supply continues to be a challenge in both quantitative and qualitative terms. Philippine educational institutions are not providing a sufficient number of suitable graduates to meet the labor demands of this rapidly growing sector.

The outsourcing industry’s surge in the Philippines has resulted in stiff competition among outsourcing suppliers and buyers alike, with the country supplying low-end bulk services in the voice sector and to a growing extent, non-voice, back-office processes. While the labor supply is adequate, applicants most suited for the work are quickly engaged, contracted, and fought over by existing outsourcing companies. This is reflected in the high attrition rates – with a base range of 30-40% – reported by many voice BPO providers.

This trend may serve as a disincentive for industry players because of the additional costs attrition entails as providers are forced to increase spending on recruitment and training efforts. With high attrition rates, companies are also at risk of repeating costs simply to retain employee bases. Further, the competition which higher attrition rates causes has the tendency to put upward pressure on salaries across the industry. Attrition is a high cost that needs a solution.

The relatively high attrition rates may also reflect the intense competition for high-quality labor in established BPO hubs. While there is a steady influx of graduates, the demand for a high-quality labor pool has been outpacing the supply in zones of high industry concentration.48

The acquisition by non-voice service providers of talent that would previously have been taken by voice-based service providers, also contributes to increasing competition for talent. This is particularly true in the country’s voice-based BPO sector in the National Capital Region (NCR) and other established hubs.

In addition, there is a large gap in the supply of mid-level managers and senior level executives. Being a relatively young and very fast-growing industry, there has not been time to nurture enough managers from within the industry to lead its large pools of young employees. To help address these issues, stakeholders have implemented intervention programs.

For example, BPAP has created a National Competency Test for three broad competency areas applicable to the IT-BPO sector (that is, problem solving, English proficiency, and computer skills). This test will be rolled out nationwide to check core competencies for suitability in the industry among students, graduates, and jobseekers. BPAP has pilot-tested this initiative in a few universities and aims to test 10,000 applicants in 2010.

Test scores will be compiled in a database from which companies can search for suitable applicants according to their needs. This would help companies narrow their recruitment efforts by allowing them to select from pretested applicants whose scores for each competency match their specific requirements. As a more efficient recruitment process, this will save companies much time and resources and thus help sustain industry growth.

Results would also show testees the competencies in which they are strong as well as those which they need to improve to be hirable.

Results will also reveal both the weak areas of schools as well as their competencies, and this information can be used to rank the schools. Schools will find out how their graduates perform on the tests allowing them to take steps to address weaknesses.

If the tests are used by only a few schools and companies, the cost will be very high. But if the IT-BPO industry and universities partner to use the test, the cost would fall dramatically, perhaps to only PhP 200 per testee (from the current cost of about PhP 500).

The effectiveness of this testing and recruitment program will depend on the extent of participation by schools and companies. Participation can be encouraged in several ways including further subsidies from government, subscriptions of companies, affordable fees from test takers, or a combination of these contributions from primary stakeholders. Awareness campaigns and logistical support would also help make the program coverage more comprehensive and the program more effective.

Another education initiative to address the supply of qualified talent, is a program developed by IBM called Service Science Management Engineering (SSME). BPAP, CICT, and IBM are working to optimize the adoption of this program in schools for the IT-BPO industry. The Commission on Higher Education (CHED), which has formed a technical consulting panel to recommend changes in the curriculum, could help speed up the adoption process. However, while CHED assigned two seats to the IT-BPO sector on the panel for IT education, BPAP was not present in any of the panel’s six meetings in 2009.

China is aspiring to be a world leader in the IT-BPO industry and is striving hard to improve its education system to cater to the needs of the BPO sector. The Chinese educational system has been very quick to adapt its curriculum to train youth in labor skills in high demand. The University of Beijing, for example, has developed a special degree program for SSME which is being replicated in other Chinese universities. This program qualifies students immediately for jobs within the sector. These initiatives in China indicate the type and level of support that countries are investing to become competitive in the IT-BPO industry; the Philippines should do no less.

Another challenge facing the IT-BPO industry is the gap between the academe and industry. While adequate numbers of graduates are produced by higher educational institutions, many graduates take courses not directly related or complementary to outsourcing. This requires companies to invest in training and retraining new hires so that skill sets better match industry needs.

In a forum convened by the Philippine Chamber of Commerce and Industry in 2007, a national sense of urgency to bridge the gap between the academe and industries in general was apparent. The forum acknowledged that the academe must drastically improve the proficiencies of graduates in the following skills sets: English, math, and science technology—the basic academic requisites needed in the outsourcing industry.

English proficiency is important even for non–call center jobs. Some potential employees are not hired because they are uncomfortable speaking in English. BPAP has found that when language-training methods used in schools are supplemented with more interactive methods that are typically used in basic training programs in IT-BPO companies, students are able to improve their English proficiency and significantly improve their chances of landing a job. However, these interactive methods can only be effectively provided in classes of no more than 25 students, a class size that is not viable for schools. In addition, classes need to be allowed to run for at least three hours at a time and schools that adopt these methods need to adjust to their class schedules to accommodate this requirement. Finally, schools need to identify teachers that can be trained in the methodology and allow them the time to train.

BPAP has rolled out an initiative called Advanced English Pre-employment Training (AdEPT) that helps schools implement the industry-based program in their curriculum. AdEPT has proved highly effective however it needs more support and cooperation from schools, companies, and other stakeholders to spread its reach and benefits.

Students also lack opportunities outside school to practice English. If students do not hear the language in their everyday lives and are not immersed in it, they cannot master English. Campaigns to increase the use of correct English in the media would go a long way in improving English proficiency on a wide scale for all Filipinos.

Greater IT literacy and access to computers could also drastically increase the number of suitable talent available to the IT-BPO industry. But computer ownership penetration in the Philippines is very low, though the number of users is 20 times higher. Most users gain access to computer and the Internet in Internet cafes and there is great potential to market or provide training programs at these sites. There is still a need, however, to increase computer ownership or access through less red tape in importing computers, discount and financing schemes, public computer centers in areas where there are no Internet cafes, and other initiatives.

Donating computers for schools for training programs (that is, science, English and math programs) would also improve education, especially in the 6,000 public high schools, most of which still lack computers. The IT-BPO industry discards large numbers of imported computers which are hard to donate directly to schools because they are required to pay duty on duty-free imported equipment not transferred to similarly privileged persons. BPAP can talk to the GRP to make an exception. The Department of Education (DepEd) is entitled to receive duty-free importation of goods.

Finally, one of the most effective ways of increasing the labor supply for IT-BPO is to sustain a comprehensive awareness campaign on the many benefits of a career in the industry. There is a mistaken general view that call center work entails a low-end and dead-end job. Hence, companies are not attracting a very large group of otherwise qualified talent. Students and the public in general should be made more aware of opportunities in the sector.

The awareness campaign could also attract talent from alternative pools such as graduate and labor pools in more remote areas of the Philippines who are not yet familiar with IT-BPO industry; retirees, housewives, and other unemployed or underemployed Filipinos; and employed persons wanting to shift careers or locations. Currently, for example, there are many Filipinos working abroad who can potentially be hired by the industry. India has already undertaken such an initiative. There is therefore an urgent need to reach out all these potential hires to inform them that the IT-BPO industry offers great career opportunities.

Policy Environment

There is no clear and consistent national policy to support the IT-BPO industry that is implemented by all levels of government. A few Philippine government agencies understand the benefits of the IT-BPO industry and support the inflow of investment, but others seek to tax companies more and create obstacles making it more difficult for firms to engage in their businesses.

For example, the scope of BIR policy on 15% income tax for skilled employees of Regional Headquarters is unclear and inconsistent. This affects potential entrants, employees, and existing companies. The BIR did not undertake a consultative process before certain policies were changed in 2009. There are also different interpretations of policies.

Another area where there can be some unanticipated cost challenges for MNC service providers is where local government units (LGUs) seek payments in apparent contradiction of PEZA guidelines. The 1991 Local Government Code gave cities and provinces authority to impose certain regulations, taxes, and fees on businesses. There has been some struggling with LGUs in regard to unclear policies, for example imposition of fees. There is no clear template on how to deal with LGU concerns. Some companies have entered into a MOA with cities to pay reasonable fees for basic city services such as garbage collection and the maintenance of peace and order. More clarity from the national level is needed and explanations given to LGUs in order to avoid misunderstandings and possible problems for IT-BPO locators, especially as they spread to more cities around the country.

Industry Promotion

The GRP does not do a very good job of international investment promotion. International outsourcing conferences hosted by the government, for instance, should be timed better and not be scheduled at the same time as other important events.

There is a need for a better public information campaign or global advertising campaign with the participation of the private sector. This is vital and timely because there currently is a window of opportunity to significantly increase the country’s market share in the global IT-BPO market.

India is saturated and much of India’s top-tier talent has already been hired by the industry or otherwise been taken up. In addition, India and other competing countries recently passed restrictive legislation and rules. Also, it is not a good business strategy to invest solely in one country. Therefore many global companies that have a large presence in India, such as IBM, are expanding and looking for alternative countries.49 The Philippines, on the other hand, has very favorable prospects. The Philippine industry needs to get together with credible organizations such as BPAP, CICT, PEZA, and the JFC to start a more active information campaign.

LGUs in China are also developing into a real threat in the non-voice outsourcing market. The behavior and incentive structure for LGUs in western China contrasts sharply with the Philippines. In China, LGUs have studied what companies require. They understand that investors find going to several offices to be inefficient. So they have built buildings where key government agencies involved in setting up a new business are represented (e.g. tax, environment, and land registry).

There is also a well-crafted incentive system for LGUs in China. LGUs earn extra funding for their cities and provinces from the central government when they demonstrate their ability to attract IT BPO companies. Hence, there is a high incentive for LGUs to be knowledgeable about the industry and to entertain potential investors. In the Philippines, there is generally an absence of LGU involvement in investment promotion and too many LGUs have even developed disincentives for investors that operate in the Philippines.

Physical Infrastructure

Internet access is not widespread. Below 12% of the 18-20 million households have access to the Internet, a figure significantly behind other countries.

There is considerable ongoing construction by telecommunication companies to improve infrastructure. Some are focusing on improving wireless Internet services to improve business continuity in times of typhoons. However, wireless cannot completely replace wired Internet connections. There is a need for an extensive higher-speed broadband network as the Philippines’ broadband infrastructure is insufficiently robust (see Part 3 Infrastructure: Telecommunications).

With the demise of the National Broadband Network (NBN) project of the GRP, the focus has been to work with the private sector to further develop the ICT infrastructure to achieve universal broadband access. CICT is formulating a broadband access plan that will increase Internet access throughout the country.

The power situation in the Philippines is at a critical level with demand nearly exceeding reliable supply. New baseload plants are needed (see Part 3 Infrastructure: Power).

PEZA was initially created to cater to companies manufacturing for export and locators receive discounted electric power. Although this may be difficult to apply to the IT-BPO sector because the companies do not share a common grid, the IT-BPO sector should explore ways of availing of this incentive.

Office Infrastructure

Rental costs are primarily driven by the market. Although there is plentiful supply of real estate for the IT-BPO sector until the second half of 2011, shortage thereafter will escalate rental rates. Many real estate developers were burned out by the oversupply created in the last three years and have ceased new construction until there is a deficit to push up their returns.

The PEZA rule on density for every seat is 70 square feet. However, some firms have gone to 50 square feet per seat. There is a need to review the PEZA rule on density as an increased density will have substantial savings. There is an 18% percent differential between a density of 70 square feet per seat and 50 square feet per seat. This has also been an issue in terms of getting permits especially in PEZA.

Exchange Rates

There could be an exchange rate at which the Philippines is no longer competitive should the peso strengthen too much and too fast. The IT-BPO sector should be vigilant and speak out against such a development. An economic advisor of the previous administration projected in early 2010 that remittances could grow to more than US$ 40 billion and 17% of GDP in five years, which could cause the peso to appreciate below PhP 40 to US$ 1. There is much debate over the future value of the peso. The industry should seek to shift to higher-value services to ensure a stable, competitive, and productive business environment supported by a good educational system and information campaign.

Footnotes

- In general, IT-BPO describes the whole outsourcing industry in the Philippines, including information technology and engineering services outsourcing (also known as ITO or ESO). ITO includes software development, applications development and management, IT infrastructure management, and sometimes technical support. ESO includes engineering design for manufacturing, industry or construction, architectural design, construction management, building management, etc. BPO refers to customer service (voice and non-voice) including back-office, finance and accounting, human resources, transcription, legal processes, also known as knowledge process outsourcing (KPO), and other non-IT or non-ESO services. Animation and game development overlap these classifications and include “creative process outsourcing” elements.[Top]

- In 2008, employment in back-office or non-voice BPO was at 72%, compared with call centers at 15%.[Top]

- Everest Research Institute, 2008[Top]

- An entry level employee earning PhP 15,000 a month pays PhP 22,500 a year in income tax. One hundred thousand new employees will pay PhP 2.25 billion. When the industry reaches one million, an estimated PhP 23 billion will be paid in income taxes, every year. If one million BPO workers spend PhP 10,000 on goods subject to a 12% VAT the government will collect PhP 14.4 billion. After expiration of ITH, firms located in PEZA zones pay 5% corporate income tax on gross revenues. The faster the industry grows, the more revenue the government collects.[Top]

- Data Protection Act XXVI of 2001.[Top]

- With the issue of the Labor Code prohibition of night work for women employees, an exception was made in the IRRs allowing women to work at night provided that safety measures are met.[Top]

- A BPAP online survey conducted February 2 to March 1, 2010 with 160 respondents showed that 34% of respondents rated the tight labor market their No.1 risk concern. To meet this concern, an increasing number of respondents said they are providing education and training.[Top]

- In India, IBM went from 4,000 to 85,000 employees in just 5 years.[Top]

{kind=link}

{kind=link}

{kind=link}